By the end of this blog, you will be able to:

- Understand money and how to raise it wisely

- Identify the three key questions you must answer before you even start looking for funding

- Understand the three major funding options available to startups, and how each one actually works

- Use a simple decision framework to figure out which funding option fits your business, your stage, and your risk appetite

- Evaluate funding strategically instead of emotionally, so you raise money on your terms, not out of panic

Picking Up Where We Left Off

In our last blog, we broke down the basics of financial knowledge, the idea was to bring business and non-business background founders onto the same page, so that terms like cash flow, equity, and revenue no longer felt intimidating. Now that we’re speaking the same language, it’s time to take the next step together: choosing how to actually fund your startup.

Introduction

Every startup needs money, but not every startup needs investors. Founders often chase funding before understanding whether they actually need it, one of the most common and most expensive mistakes in the startup world. Before accepting an investor’s cheque or signing off on a loan, take the time to understand how the option works, what it costs, and how it affects your ownership and growth. Money doesn’t just fuel your business, it also attaches strings, and the type of string matters just as much as the amount.

Three Questions You Must Answer Before Discussing Funding Options

You need to get honest answers to three questions. Whether it’s with a bank, an investor, or savings, whenever the discussion of optimal options arises, here’s what you should go through:

1. How much money do I actually need?

This sounds obvious, but most founders either overestimate or underestimate this number. Raising too little means you’ll be back asking for more before you’ve proven anything. Raising too much means giving away more ownership or taking on more debt than necessary. The goal is to calculate a realistic number based on your actual plans, not a round figure that “feels right.”

2. Why do I need this money?

Money without a purpose is a liability, not an asset. Are you raising funds to buy equipment, to run marketing campaigns, or to develop software? Each of these purposes comes with a different timeline for returns. Equipment might pay off over years, marketing might show results in weeks, and software development might take months before it generates revenue. Knowing the “why” helps you match the funding type to the actual use of that money.

3. How much risk am I willing to take?

This is the question founders skip most often, and it’s usually the one that comes back to bite them. Every funding option carries a different kind of risk. You might lose a percentage of ownership, you might be locked into monthly repayments regardless of how your business is performing that month, or you might have to grow slower than you’d like because you’re relying only on your own money. None of these risks are inherently bad, but you need to know which one you can actually live with before you sign anything.

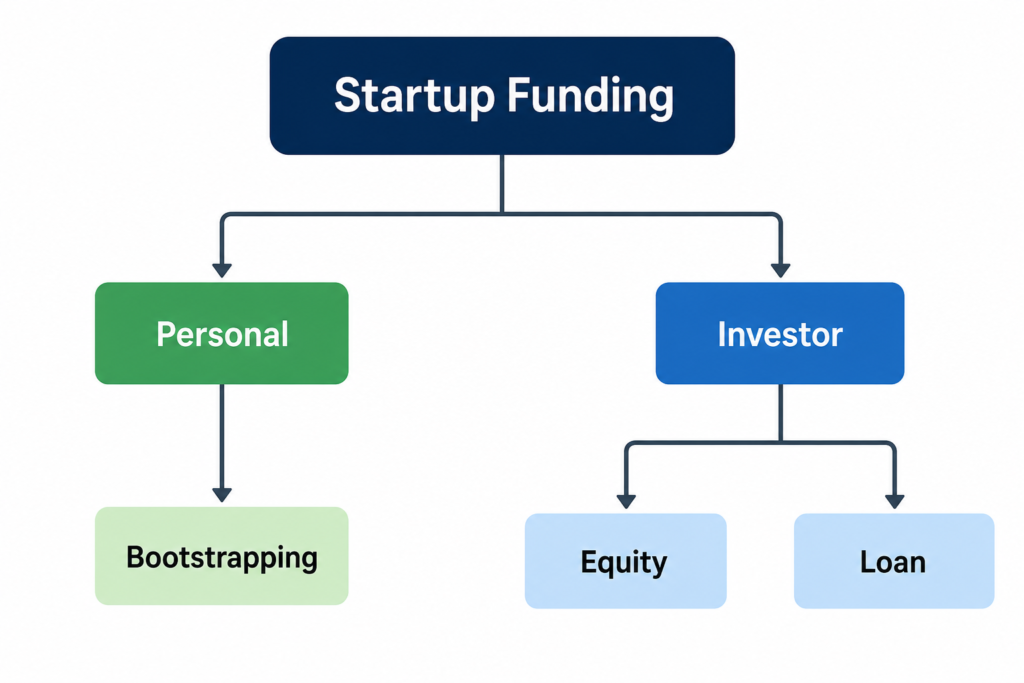

The Three Major Options of Funding

Once you’ve answered those three questions, you’re ready to look at your actual options. Broadly, every startup founder chooses from three paths.

Bootstrapping

Bootstrapping means funding your business using your own personal finances or the profits your business is already generating. There’s no bank, no investor, and no outside party involved. You save your own money, reinvest whatever the business earns, and grow at a pace that your finances allow. The biggest appeal of bootstrapping is control, you own 100% of your company and you don’t owe anyone anything. The tradeoff is that growth is often slower, and you’re limited by how much capital you personally have access to.

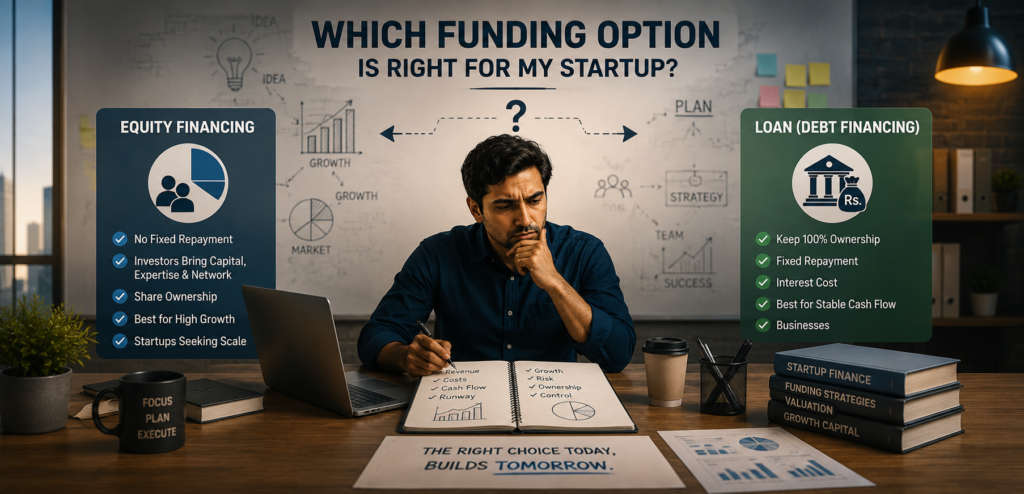

Debt Financing

Debt financing sounds more “financial,” but the concept is simple. You borrow money, usually from a bank or a lender. You promise to repay it over time with interest. Think of it the same way you’d think of a car loan or a mortgage. The lender doesn’t get a share of your company, they just want their money back, plus a fee for lending it to you. This means you keep full ownership of your business. But you also take on an obligation that doesn’t disappear just because your business had a slow month. Repayments are due whether you made a profit or not.

Equity Financing

Equity financing works completely differently. Instead of borrowing money, you sell a percentage of your company to an investor in exchange for capital. That investor now owns a small piece of your business. In most cases, they benefit when your business grows in value. There’s no monthly repayment hanging over your head, which sounds appealing. But the cost isn’t measured in interest, it’s measured in ownership and control. You now have a partner in your business decisions, even if you didn’t have one before.

A Decision Framework: Which One Fits You?

Here’s where the three questions from earlier and the three funding options come together.

Choose bootstrapping if your business requires little capital to get started, if you want to retain complete ownership, if you’re comfortable growing gradually rather than rapidly, and if you have substantial personal savings to rely on.

Choose debt financing if; your business has predictable and steady revenue, you are confident you can make consistent repayments even during slower periods, and if keeping full ownership of your company matters more to you than avoiding monthly obligations.

Choose equity financing if; your business needs significant capital that neither savings nor loans can realistically cover, the business model allows for rapid scaling, or you’re genuinely comfortable sharing ownership and decision-making with someone else. In early stages of a company, equity financing is suitable because of less accountability and commitment.

Closing Thoughts

The best financing option isn’t necessarily the one that gives you the most money. It’s the one with the lowest overall cost for your startup’s goals and your personal risk profile. A large investment that costs you a third of your company might be far more expensive in the long run than a smaller loan you could have repaid comfortably.

The goal of this blog was simple, to teach founders to evaluate funding strategically rather than emotionally. Money will always be tempting when it’s offered. The founders who build lasting businesses are the ones who pause and ask the right questions. Always choose funding that actually fits, not just funding that’s available.