By the end of this blog, you will be able to:

- Understand where your startup’s money comes from, where it goes, and where it should grow

- Read the three core financial statements without needing an accounting degree

- Track your burn rate and runway so you never get blindsided by a cash crunch

- Understand breakeven point and why reaching it changes everything for your business

- Grasp unit economics and why “making sales” isn’t the same as “making money”

- Get a basic grip on funding, forecasting, budgeting, and taxes

- Know the core KPIs every founder should track, month after month

I have a business idea. Now how do I handle money without having an MBA or an accounting degree? If that question has been on your mind while you build, you’re not alone — and this is going to be the longest article in this series, because finance is the topic that scares beginners with non-business backgrounds the most. It sounds technical, full of jargon, and like something you need a degree to even approach.

Here’s the reassurance before we start: you are not here to become an accountant. You are here to become a founder. You don’t need to master debits and credits — you need enough financial literacy to make smart decisions, avoid the mistakes that kill startups, and know when to bring in a professional. That’s exactly what this blog is designed to give you. Let’s get into it.

Why Every Founder Misunderstands Finance

Here’s an uncomfortable truth: most startups don’t fail because the product was bad — they fail because the founders ran out of money before reaching profitability. A great product with poor financial management can die quietly, while a mediocre product with disciplined money management can survive long enough to improve and win. Finance isn’t a “back office” function you ignore until you’re bigger — it’s survival.

The good news is that startup finance, at the founder level, comes down to understanding three simple things:

- Where money comes from — your revenue streams, funding, investors, customers.

- Where it goes — your costs, salaries, rent, tools, marketing spend.

- Where it grows — which outflows actually generate more revenue or value, so you know where to double down and where to cut.

Everything else in this blog is a deeper, structured way of answering these three questions.

Understanding the 3 Financial Statements

Every business, no matter how small, tells a financial story through three statements. Learn to read these and you’ll understand your business better than most founders ever do.

The Income Statement.

Often called the Profit & Loss statement (P&L), its job is simple: it tells you how much money your business actually made over a period of time — a month, a quarter, a year. The logic follows a simple chain:

Revenue − Cost = Gross Profit Gross Profit − Expenses = Profit

An income statement shows whether your business made a profit or a loss over a specific period. It starts with your revenue (total sales), subtracts the cost of goods sold (COGS) to calculate gross profit, and then deducts operating expenses such as rent, salaries, marketing, and software. One lesson every founder should remember is that revenue is not the same as profit. A business can generate high sales but still lose money if its expenses are too high.

After operating expenses, you add any other income and subtract other expenses to calculate profit before tax. Once taxes are deducted, the final figure is net profit—the amount your business actually keeps or reinvests. This is the number that founders, investors, and lenders pay the closest attention to because it clearly shows whether the business is making money or losing it.

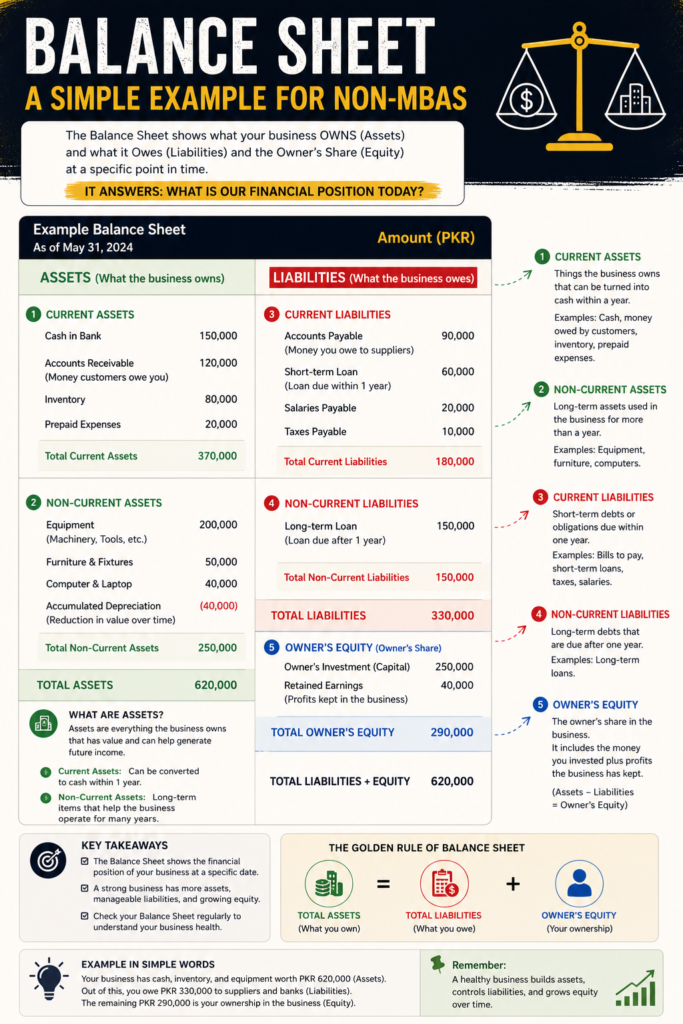

The Balance Sheet.

If the income statement shows how your business performed, the balance sheet shows where it stands at a specific moment — a snapshot investors, banks, and partners use to assess your business’s health before committing money. It answers three questions: what the business owns (assets, including receivables — money owed to you by customers), what it owes (liabilities, including payables — money you owe suppliers or lenders), and what belongs to the owner once everything is settled (owner’s equity):

Assets = Liabilities + Owner’s Equity

Everything the business owns is financed either by debt or by the owner’s own stake.

Think of a balance sheet as a snapshot of your business’s financial position. Your assets include everything your business owns, divided into current assets (cash, receivables, inventory, and prepaid expenses) and non-current assets (equipment, furniture, and computers). Your liabilities are what your business owes, split into current liabilities (supplier invoices, short-term loans, salaries, and taxes) and non-current liabilities(long-term loans).

The difference between total assets and total liabilities is the owner’s equity, which represents the owner’s investment plus retained profits. This is why every balance sheet follows the equation Assets = Liabilities + Owner’s Equity—everything the business owns has been financed either through borrowed money or the owner’s investment. A financially healthy business gradually grows its assets, keeps liabilities under control, and increases its equity over time.

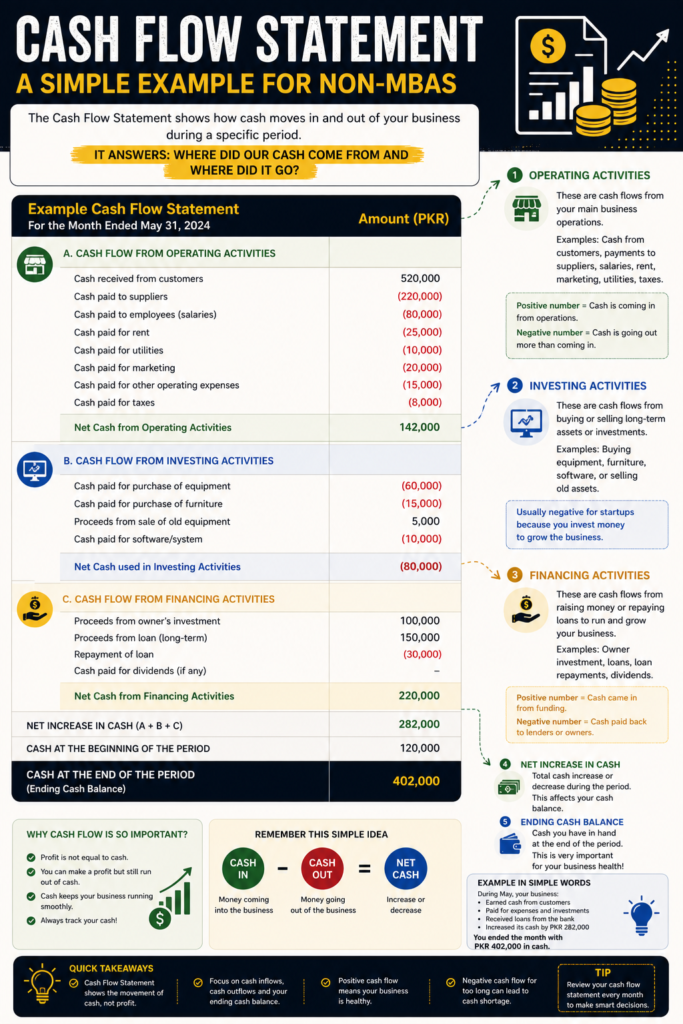

The Cash Flow Statement.

Of the three, this is the one a founder should obsess over most. It tracks the actual movement of cash in and out of your business — a business can look profitable on paper and still collapse from running out of cash in the bank. This happens often: you might invoice a client and technically “earn” revenue, but if they haven’t paid yet, you can’t use that money for rent or salaries next week. Many profitable businesses die not from a lack of profit, but from running out of cash at the wrong moment.

Picture a month in three buckets: operating (cash from customers minus payments to suppliers, staff, rent, and taxes), investing (cash spent on or earned from equipment or software — usually negative for startups, since you’re investing to grow), and financing (cash from owner investment or loans, minus repayments). Add all three to get your net increase in cash; add that to your starting cash for your ending balance — the actual money in the bank. Remember: cash in minus cash out equals net cash, and profit isn’t the same as cash.

Burn Rate vs Runway

Burn rate and runway are two terms you’ll hear constantly, and together they answer one of the most important questions a founder can ask: how much time do we have left?

Burn rate is the amount of cash your business spends every month. If monthly expenses total $10,000 and revenue doesn’t yet cover that, burn rate reflects how much of your reserves get eaten into each month. Tracking this gives you an early warning system — if it spikes, you need to know why immediately, not three months later.

Runway tells you how much time you have before you run out of money completely:

Runway = Cash Available ÷ Monthly Burn Rate

If you have $60,000 in the bank and you’re burning $10,000 a month, your runway is 6 months. This number should shape almost every major decision you make — hiring, marketing spend, or when to start fundraising. Founders who don’t track it often find themselves fundraising in a panic, with little leverage and even less time.

Breakeven Point

Your breakeven point is the moment your revenue exactly equals your total costs — you’re not losing money, but not making a profit either.

Reaching breakeven typically requires increasing revenue (more customers, higher prices, better retention), reducing costs (leaner operations, smarter spending), or usually both. Once you cross this point, every additional dollar of revenue, minus its direct costs, starts contributing to actual profit instead of just covering what you already owe — often a genuine turning point where growth starts compounding in your favor.

Unit Economics

Unit economics simply means understanding whether you make or lose money on a single unit of your product or service — one customer, one sale, one transaction. It strips away the complexity of the overall business and asks: for one unit, does the math work?

Here’s a simple example: you run a small bakery and sell a custom cake for $50. Ingredients, packaging, and delivery cost $30, leaving a $20 profit per cake. Now say you spent $25 on ads to get that customer to order. Suddenly that “profitable” cake is only making you $5 — or if the ad cost $35, you actually lost money on the sale. This is why some startups look busy and full of customers while quietly bleeding money: nobody checked whether each unit was truly profitable once every cost, including acquiring the customer, was counted.

Funding vs Equity

At some point, most founders consider raising outside money — which raises the question of funding versus equity: how much should you raise, and how much ownership are you willing to give up for it? This topic, involving valuation, dilution, and investor rights, deserves its own discussion — we’ll cover it in depth in the next blog. For now, just know that every dollar you raise from an investor typically costs you a slice of ownership, and that trade-off should never be made lightly.

Forecasting

Forecasting is the practice of estimating your business’s future — revenue, expenses, cash needs — based on the information and trends you have today. It’s one of the more technical parts of running a business, especially demand forecasting (predicting how much customers will actually want to buy).

For a founder, forecasting turns guesswork into planning. It helps you anticipate whether you’ll need to raise money before your runway ends, whether to hire now or wait, and whether your growth plans are realistic. In practice, it’s done by looking at historical data (if you have any), market trends, and reasonable growth assumptions, then projecting these forward. It won’t be perfectly accurate — no forecast ever is — but its purpose isn’t perfection, it’s to give you an informed view of what’s coming so you can prepare instead of being surprised.

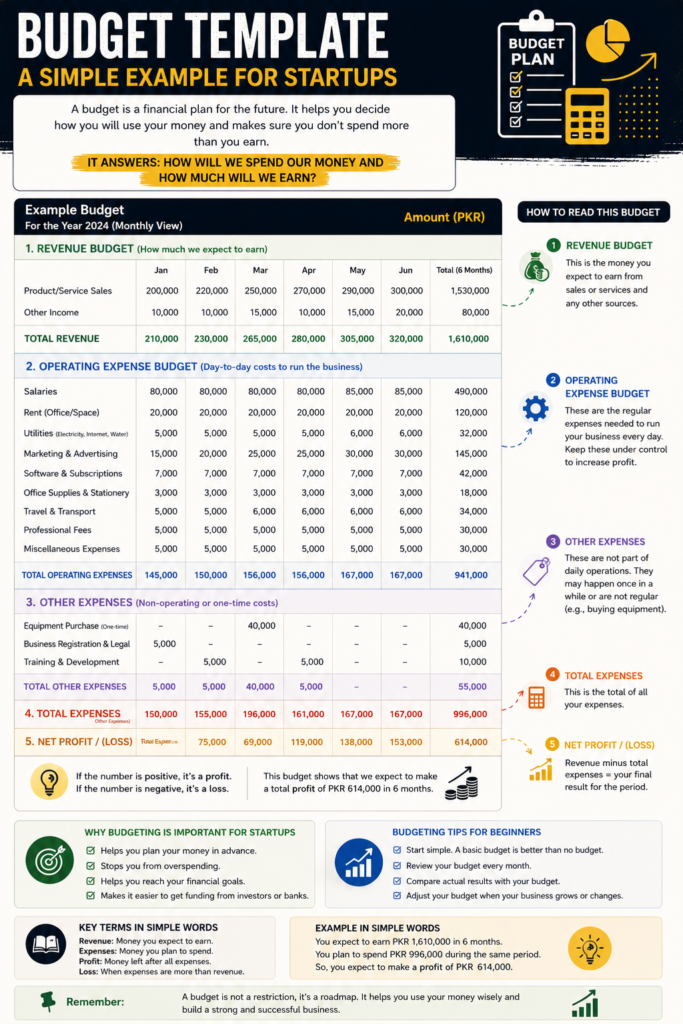

Budgeting

Startup budgeting turns your financial forecast into an action plan. While forecasting estimates future revenue and expenses, a startup budget decides how you’ll use your money to reach those goals. Founders typically build a budget using projected revenue and available cash, then allocate funds across product development, marketing, salaries, and daily operations. A well-planned budget controls spending and keeps your startup focused on its highest priorities.

A budget also improves financial decision-making. Before hiring new employees or increasing marketing spend, it helps you answer a simple question: Can we afford it? Regular budget reviews quickly reveal overspending, cash flow issues, or unrealistic revenue expectations. Department-level budgets also improve accountability, while a consistent budgeting process demonstrates financial discipline to investors and lenders.

A typical startup budget lists expected revenue, subtracts operating and one-time expenses, and estimates the net profit or loss for each month. A positive result shows that your business is moving in the right direction, while a negative result gives you time to adjust before problems grow. When you review and update your budget every month, it becomes a practical financial roadmap that supports smarter business decisions and sustainable growth.

Taxes

Taxes feel irrelevant when you’re just starting out, but they become critical the moment you scale — and getting them wrong can be costly, especially in Pakistan’s regulatory environment, where registration and compliance rules are strictly enforced. As a first-time founder, you don’t need to become a tax expert, but you do need working awareness of three taxes in particular.

Income Tax is the one every profitable business eventually deals with — a tax on your actual profits. As your startup grows and starts earning consistently, this becomes a recurring obligation you need to plan and set money aside for.

Sales Tax matters because founders need to know exactly when they must register for it and start collecting it from customers. Many assume this only applies to large companies, but depending on your revenue, industry, and province, the registration threshold can arrive sooner than expected — and failing to register when required brings penalties, not just back-taxes.

Withholding Tax is the one most founders unknowingly get wrong. Businesses must deduct this tax at source on certain payments — to vendors, service providers, or employees — and deposit it with tax authorities on their behalf. It’s easy to overlook, so many founders violate these requirements without realizing it. The safest approach: the moment you start paying vendors or contractors regularly, talk to a tax consultant about your withholding obligations.

You don’t need to handle taxes yourself — but you do need to know these three exist and when to bring in professional help.

Important KPIs Every Founder Should Know

Beyond the statements and concepts above, there are a handful of numbers you should check every month.

Monthly Revenue — total money earned in a month; your basic pulse check on growth and demand.

Monthly Expenses — total money spent in a month, across every category; tracked alongside revenue, it shows whether you’re moving toward or away from profitability.

Gross Profit — what’s left after subtracting the direct cost of delivering your product from revenue; shows how efficiently you deliver what you sell, before overheads.

Gross Margin — gross profit as a percentage of revenue, letting you compare efficiency over time or against competitors regardless of scale.

Net Profit — your true bottom line, what’s left after every expense including overheads, taxes, and interest. This is the number that tells you if your business is sustainable.

Net Margin — net profit as a percentage of revenue, giving a clean, comparable sense of overall profitability.

Together, these KPIs give you a monthly report card for your startup. You don’t need fancy software to track them — a simple spreadsheet, updated consistently, is enough to start making informed decisions instead of guesses.

Bringing It All Together

Startup finance may seem overwhelming at first, especially if you don’t have a business background. But in reality, it’s about building a few simple habits: know where your money comes from, where it’s going, keep an eye on your cash flow, and review your numbers regularly. For more technical areas like taxes or financial forecasting, don’t hesitate to seek professional advice.

You don’t need an MBA or an accounting degree to build a financially successful startup. You simply need the discipline to understand your finances and make decisions based on them. That’s the mindset of a successful founder—and in the next part of this series, we’ll explore two of the most important startup finance topics: funding and equity.